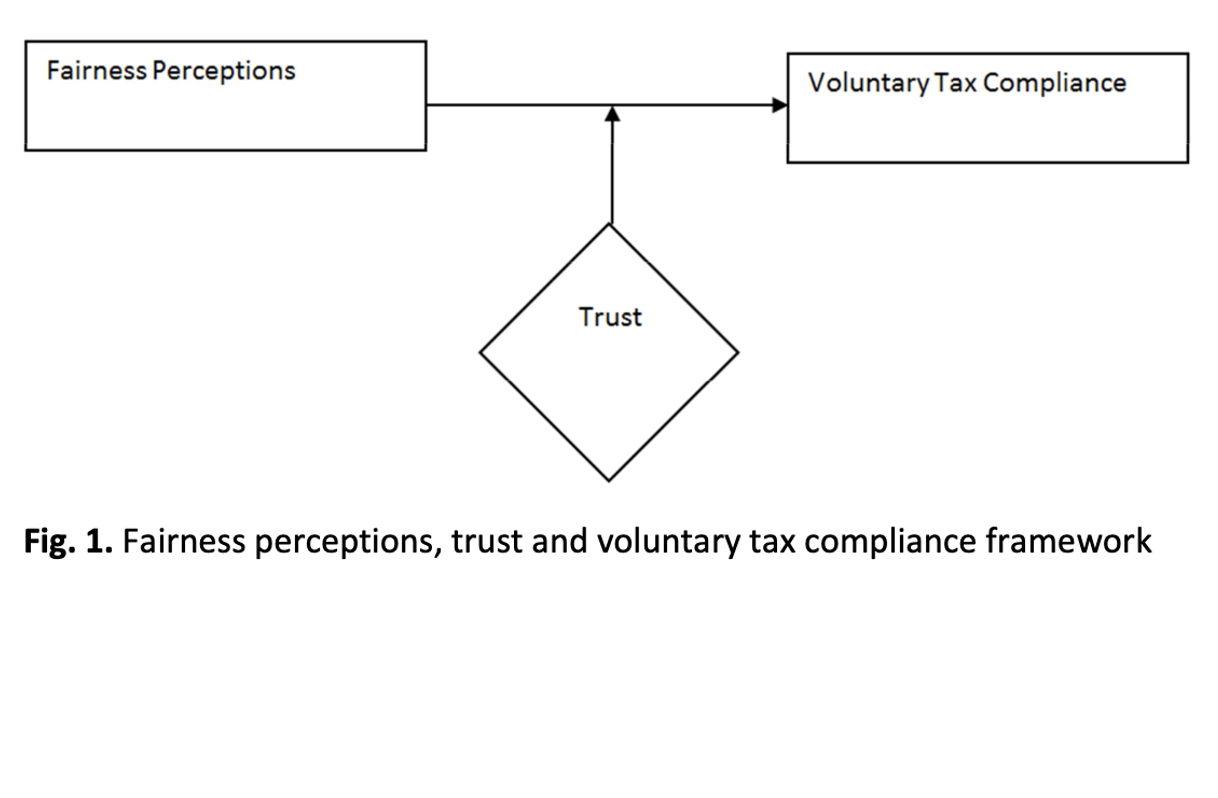

Trust as Moderating Variable in the Relationship between Fairness Perceptions and Voluntary Tax Compliance in Nigeria: A Theoretical Framework

Keywords:

voluntary, tax, trust, income, compliance, fairness perceptionsAbstract

This paper presents a theoretical framework on the moderating effect of trust in the

relationship between fairness perception and voluntary tax compliance in Nigeria.

The variables proposed under examination are fairness perceptions; trust in authority

and voluntary tax compliance. If validated the model would have significance

important policy implications to the Nigerian government and other stakeholders.

The model would also serve as a basis for reference to other researchers willing to

undertake study in the same area.

Downloads

Published

2020-10-24

How to Cite

Ya’u, A., & Saad, N. (2020). Trust as Moderating Variable in the Relationship between Fairness Perceptions and Voluntary Tax Compliance in Nigeria: A Theoretical Framework. Journal of Advanced Research in Business and Management Studies, 10(1), 28–39. Retrieved from https://akademiabaru.com/submit/index.php/arbms/article/view/1284

Issue

Section

Management studies